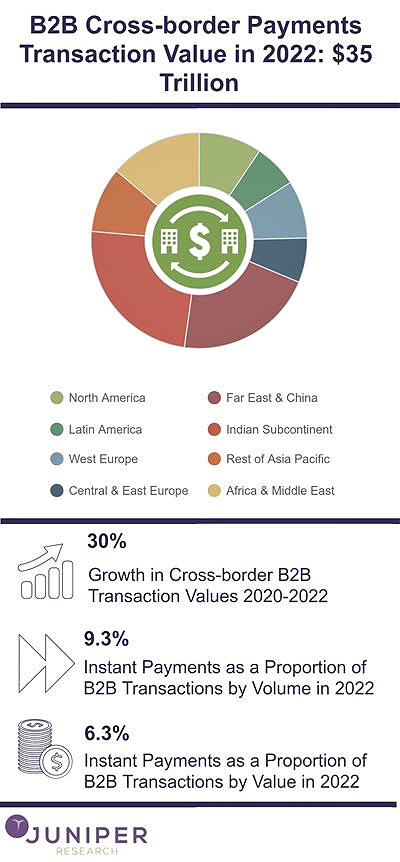

A new study from Juniper Research predicts the total value of B2B cross-border payments will reach $35 trillion in 2022 from a COVID-related low of $27 trillion in 2020. This 30% growth will take two years for recovery following the devastating economic impact of the coronavirus pandemic.

The report says businesses will be cost-conscious particularly on new spending and in order to recover lost business and regain growth, cross-border payment vendors must offer compelling cost propositions to companies or they will fail to recover lost traffic.

Instant payments will grow, but slowly

Despite the obvious benefits to business, Juniper Research says instant payments, which typically settle within 10 seconds, will account for 9.3% of B2B transactions by volume in 2022, up from 6% in 2020.

These instant payment transactions however will only account for 6.3% of B2B transactions by value, primarily because they are limited to lower-cost transactions.

Real value of instant payments is future capability

While the short-term value of instant payments appears lower, it’s the new capabilities in the longer term that could have much bigger value.

“Instant payment schemes are built on ISO 20022, which unlocks additional messaging capabilities. These can be used to inject transparency and build new services such as automation, which will add significant value to complex accounts payable processes,” Juniper Research report author Nick Maynard said.

Three key trends in B2B payments

In a companion whitepaper, Juniper Research identifies three key trends revolutionizing B2B payments including:

- Increased automation – in order to increase speed, reduce costs and minimize errors, expect to see increased use of electronic invoice capture and invoice automation; simplified invoice approvals; software integration; and new ways to manage cash flow.

- Blockchain payment implementation – while still in the early stages, blockchain technology offers increased transparency, faster speed, reduced complexity and errors, and increased security. Visa B2B Connect and RippleNet are two promising developments.

- Implementation of instant payments – real-time payments are disrupting the marketplace, but the US is lagging behind other countries. Already years behind some real-time payment platforms in Europe, such as SEPA Instant Credit, the US market is playing catch-up on instant payments.

These are encouraging signs of innovation in the cross-border B2B payments sector, but real-time payments and the benefits of its implementation can’t come soon enough for pandemic-challenged economies.